Highlights

- Global semiconductor sales hit a record $99.5 billion in March 2026, up 79.2% year-on-year, with AI chips projected to account for roughly half of $975 billion industry sales in 2026.

- The Roundhill Memory ETF (Nasdaq: DRAM) reached $10 billion in Assets in just 43 days—the fastest pace ever for an exchange-traded fund—signalling acute Scarcity in high-bandwidth memory chips critical to AI.

- Nvidia (NASDAQ: NVDA), TSMC (TSM), Broadcom (NASDAQ: AVGO), AMD (NASDAQ: AMD), ASML (NASDAQ: ASML) and Micron (NASDAQ: MU) are anchoring what analysts compare to the dotcom era in Capital intensity and sector concentration.

The Scale of Demand

The global semiconductor industry is on track to reach approximately $975 billion in sales in 2026, representing about 26% year-on-year growth and marking the first time the sector approaches the $1 trillion milestone. This expansion is primarily driven by the AI infrastructure boom, with generative AI chips alone expected to contribute nearly half of total industry Revenue.

According to the U.S. Semiconductor Industry Association, global semiconductor sales reached $99.5 billion in March 2026, surging 79.2% year-on-year to set a new all-time record.

With AI infrastructure spending expected to reach around $660 billion in 2026 alone, TSMC is benefiting from surging demand for advanced chip Manufacturing. The company reported Q1 2026 revenue of $35.9 billion, up nearly 39% year over year, while AI high-performance computing has grown from about 46% of revenue in Q1 2024 to roughly 61% in the latest quarter.

The Memory Bottleneck

The most striking development is the emergence of memory chips as the critical constraint. The Roundhill Memory ETF (DRAM) hit $9.8 billion in assets under management in 43 days—the fastest pace ever for an exchange-traded fund. The CEO of Roundhill Investments told CNBC that rapid growth is tied to the limited number of companies involved in producing high-bandwidth memory or DRAM chips, which are considered integral to the artificial intelligence revolution.

Dave Mazza, CEO of Roundhill Investments, stated: "Investors are waking up to the fact that the biggest bottleneck in the AI build-out is actually memory chips. There's an incredible amount of Supply and demand imbalance with memory."

This constraint reshapes the Investment thesis. If logic chips (GPUs) are the accelerators, memory is the fuel tank—and global capacity to produce high-bandwidth memory at scale is severely limited.

Supply Chain Concentration and Geopolitical Risk

TSMC, the world's largest foundry, produces chips for Nvidia, Apple, AMD, and many other major customers, making it one of the most strategically important companies in the semiconductor industry. Its advanced 3nm, 5nm, and 7nm nodes account for 74% of wafer revenue, and AI accelerator revenue is forecast to grow at a compound annual rate of 54% to 56% through 2029.

The concentration creates both opportunity and risk. TSMC expects 2026 capital expenditures to be between $52 billion and $56 billion, with a significant portion directed toward expanding leading-edge nodes and advanced packaging capacity. Analysts expect the company's revenue to rise from around $163.9 billion in 2026 to roughly $311.5 billion by 2030, implying revenue could almost double within four years.

But Taiwan's central role makes geopolitical risk unavoidable. Any disruption to Taiwan Strait shipping or export controls would cascade through global AI infrastructure buildouts.

Dotcom Comparisons and Valuation Risk

The comparison to late-1990s excess has become unavoidable. The semiconductor sector continues to absorb capital at a pace tied to the AI infrastructure buildout. Supply-chain investments in the US, Europe, and Asia are mitigating some geopolitical risk, while process shrinks to 2nm and HBM4 ramp-ups promise efficiency gains.

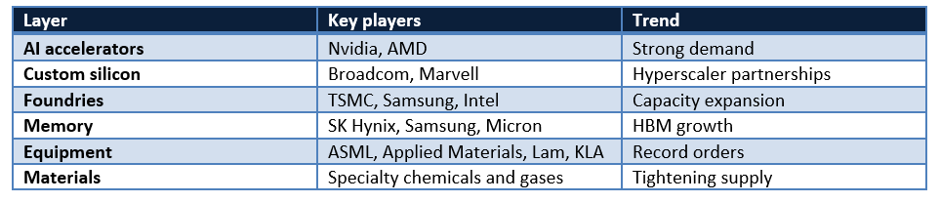

Yet the demand drivers appear structurally different from dotcom. With hyperscaler capex approaching $700 billion, the biggest opportunities are concentrated across a small number of companies controlling critical layers of the AI chip supply chain, from ASML's EUV machines and TSMC's advanced manufacturing to Nvidia's GPU ecosystem, Broadcom's custom AI silicon, and Marvell's data centre interconnects.

The question is not whether AI demand is real, but whether current valuations and growth expectations are sustainable through inevitable cycles of capex saturation and Margin compression.

Investment Dynamics and ETF Flows

For investors who prefer Diversification over single-stock concentration, the VanEck Semiconductor ETF (SMH) offers a practical alternative. The fund charges a 0.35% expense ratio and has roughly $46 billion to $47 billion in assets.

The VanEck Semiconductor ETF rallied nearly 4% to build on a nearly 49% rally in 2025, posting its third straight year of gains and best year ever in 2023 when it gained more than 72%.

The speed of ETF inflows signals how quickly institutional capital is flowing into the sector. When a specialist memory ETF reaches $10 billion in 43 days, the market is pricing both genuine scarcity and elevated expectations for perpetual growth.

Please wait processing your request...

Please wait processing your request...