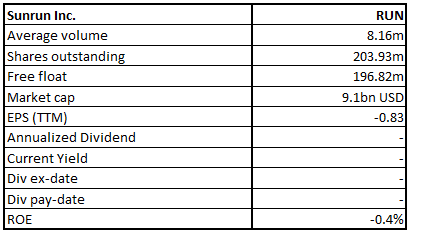

Sunrun Inc.

RUN Details

Sunrun Inc. (NASDAQ: RUN) is the top solar company player in the U.S with an entire focus on the residential solar systems. It provides home solar, battery storage, and energy services to its customers present across 175 cities in 22 states and Puerto Rico.

FY20 Results Performance (For the Year Ended 31 December 2020)

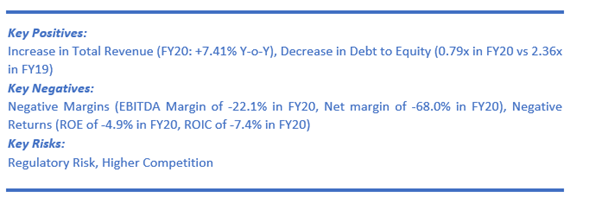

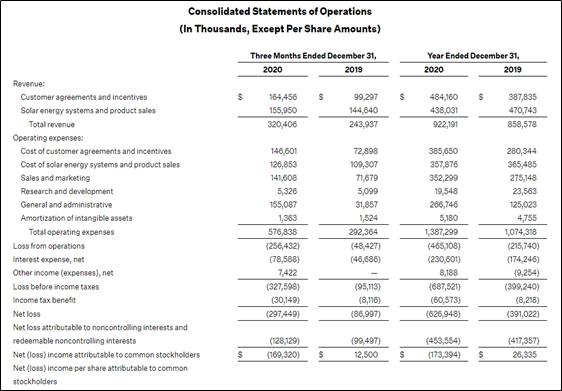

Total revenue during the period increased by 7.41% YoY to $922.19 million and the customers’ additions remained healthy at 84,559, which also includes subscriber additions of 70,774. This takes the total customers’ to 550,078, including 478,910 subscribers. Solar energy capacity installed during the year stood at 603 Megawatts while that for subscribers was 511 megawatts. Total operating expenses for the period increased by 29% YoY to $743.5 million.

Consolidated Financial Snapshot (Source: Company Reports)

Q1FY21 Results Performance (For the Period Ended March 31, 2021)

RUN has logged a strong revenue growth of 59% YoY to $334.8 million. The customer additions remained healthy as it added 23,556 customers, including 20,087 subscriber additions that took its customer base to 573,634 as of March 31, 2021. It has reported annual recurring revenue from subscribers of $683 million with average contract life remaining of 17 years as of March 31, 2021. The total value generated during the period was $164.7 million. Operating expenses for the period increased by 88% to $513.3 million. Net loss attributable to common stockholders stood at $23.8 million.

Outlook

There are huge opportunities in the solar industry. As of now, mere 3% of the 77 million addressable homes have solar power in the USA. Residential electricity market in the USA is of over $187 billion per year. With its reputation of being a major player in the solar industry and focus on residential solar systems, the company is well-positioned to capitalize on opportunities in the industry.

The management has raised the growth guidance in solar energy capacity installed to 25% to 30% from its earlier prediction of 20-25% growth for 2021. Additionally, it now expects to achieve a total value generated of over $750 million in 2021 as against its earlier guidance of $700 million. However, it reiterated garnering cost synergies of $120 million run-rate by the end of 2021.

Key Risks

The company’s operations are exposed to risks of uncertainties like one caused by the outbreak of COVID-19 on the business and operations as well as the effective integration of Vivint Solar, fluctuations in the electricity production retail prices, among others.

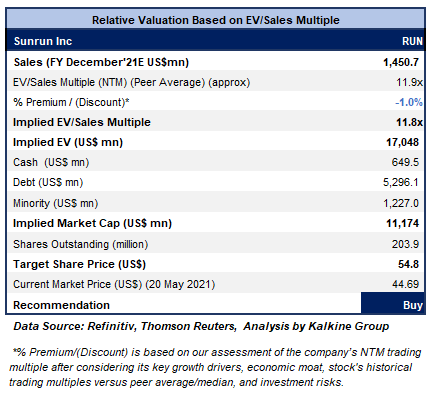

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

After three consecutive weeks of selling, the stock has taken breather having closed stronger for the ongoing week at $44.69. The technical indicator RSI with a reading around 42 and a curve at the end pointing up, suggests neutral to up momentum for the stock.

Going forward, the stock may have resistance around the 50% retracement level of $54.53 whereas support could be around the weekly low of $38.10.

Stock Recommendation

The stock declined by ~7.3% in 1 month. It has made a 52-week low and high of $15.3600 and $100.9300, respectively.

We have valued the stock using an EV/Sales multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We have applied a slight discount to EV/Sales Multiple (NTM) (Peer Average) considering its higher operating costs, negative earnings in Q1FY21 as well as higher debt levels. For the purposes of relative valuation, we have taken peers like Vicor Corp (VICR.OQ), Beam Global (BEEM.OQ), among others.

Considering the upgrade in guidance along with expanding market reach, healthy liquidity position, and decent growth outlook, we give a “Buy” recommendation on the stock at the current market price of US$44.69 per share, up by 6.68% on 20th May 2021.

Note: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Kalkine Equities LLC provides general information about companies and their securities. The information contained in the reports, including any recommendations regarding the value of or transactions in any securities, does not take into account any of your investment objectives, financial situation or needs. Kalkine Equities LLC is not registered as an investment adviser in the U.S. with either the federal or state government. Before you make a decision about whether to invest in any securities, you should take into account your own objectives, financial situation and needs and seek independent financial advice. All information in our reports represents our views as at the date of publication and may change without notice.

Kalkine Media LLC, an affiliate of Kalkine Equities LLC, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...