Adicet Bio Inc

Adicet Bio, Inc. (NASDAQ: ACET) is a clinical-stage biotechnology company. It is engaged in advancing a pipeline of off-the-shelf gamma delta T cells, engineered with chimeric antigen receptors (CARs), to facilitate durable activity in patients. Its lead product candidate, ADI-001, a first-in-class allogeneic gamma delta T cell therapy expressing a CAR targeting CD20, is being developed for the potential treatment of autoimmune diseases.

Recent Business and Financial Updates

Technical Observation (on the daily chart):

Adicet Bio, Inc. (ACET) continues to demonstrate meaningful strategic and clinical advancement despite its current technical weakness, supported by strengthening fundamentals, expanding therapeutic validation, and a materially extended cash runway. The company reported improving financial efficiency with narrower quarterly losses, reduced operating expenses, and a fortified balance sheet following a USD 74.8 million capital raise that extends liquidity into the second half of 2027. Clinically, ACET delivered highly encouraging Phase 1 results for its lead asset ADI-001 in lupus nephritis and systemic lupus erythematosus, showing consistent clinical responses, renal improvement, and a favourable safety profile—positioning the program for pivotal-stage progression in 2026. In parallel, pipeline expansion into oncology through ADI-212 and the broadening of ADI-001 into additional autoimmune indications signal a robust multi-asset development trajectory. While the share price remains under technical pressure, oversold momentum indicators at current levels coincide with substantive operational progress, creating a fundamentally supportive backdrop for long-term value accretion as ACET advances its differentiated gamma-delta CAR-T platform toward late-stage clinical development.

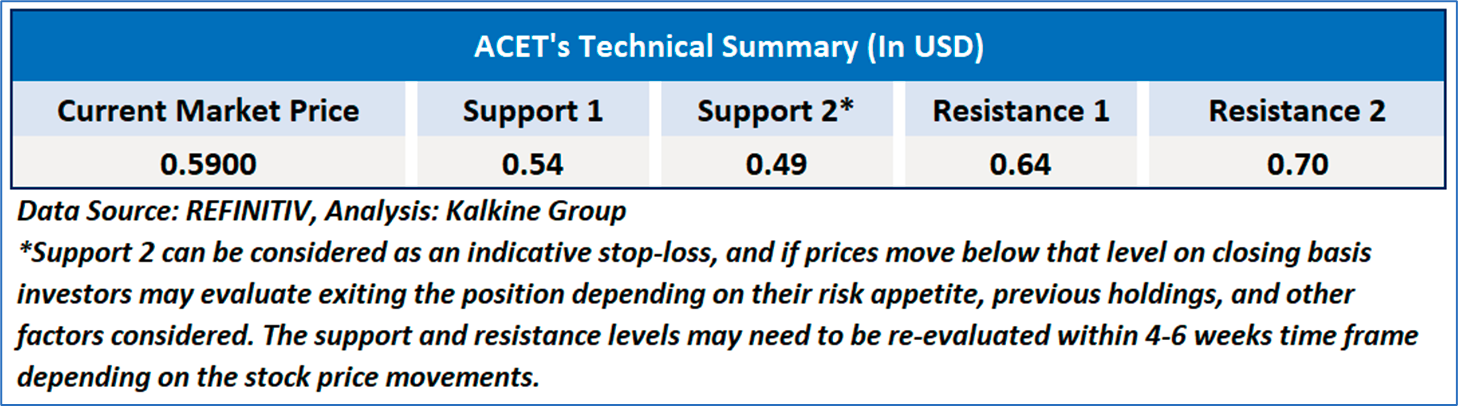

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Speculative Buy’ rating has been given Adicet Bio, Inc. (NASDAQ: ACET) at the closing price of USD 0.59, as of November 17, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is November 17, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Kalkine Equities LLC, with Delaware File Number 4697384, Foreign Qualification Registration in California File Number 202109211078, and Texas File Number 805521396, is authorized to provide general advice only. The information on https://kalkine.com/ does not take into account any of your investment objectives, financial situation or needs. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. The link to our Terms and Conditions and Privacy Policy has been provided for your reference. On the date of publishing the reports (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...