What is arbitrage?

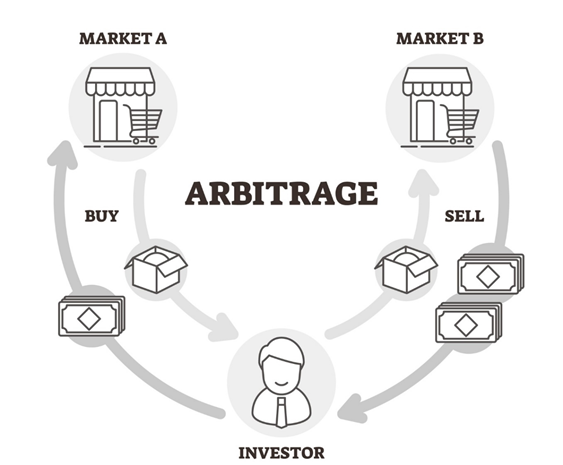

Arbitrage is a strategy that is used for exploiting the market inefficiencies for making profits. The strategy generates income by identifying a difference between the ask and the bid prices of similar or identical assets. It is a well-documented strategy that is used by all kinds of investors from new investors to fund managers. It based on the concept of buying at low prices and selling at higher prices. Generally, an arbitrage involves buying the asset from one market at lower prices and selling the same asset in another market at higher prices or selling in the same market, but at a different time. The difference between the selling and the buying price is the profit made by the trader.

What is Index arbitrage?

Index arbitrage is a type of arbitrage trading that involves making a profit by locating a difference between the actual price and the predicted price of the stock. The trader makes a profit by exploiting the inefficiencies in the market. The index arbitrage needs to be conducted in a very short span of time as price difference generally occurs because the relevant information is not reflected in the stock prices.

Few traders refer to the index arbitrage as basic trading. It is mostly used in conjunction with the day trading strategy. To identify the market inefficiencies, program trading techniques are utilised by the traders which analyse the indexes along with the future contracts.

Summary

- Arbitrage is a strategy that is used for exploiting the market inefficiencies for making profits.

- Index arbitrage is a type of arbitrage trading that involves making a profit by locating a difference between the actual price and the predicted price of the stock.

- The trader makes a profit by exploiting the inefficiencies in the market.

- The index arbitrage needs to be conducted in a very short span of time as price difference generally occurs because the relevant information is not reflected in the stock prices.

- Few traders refer to the index arbitrage as basic trading.

Frequently Asked Questions (FAQs)

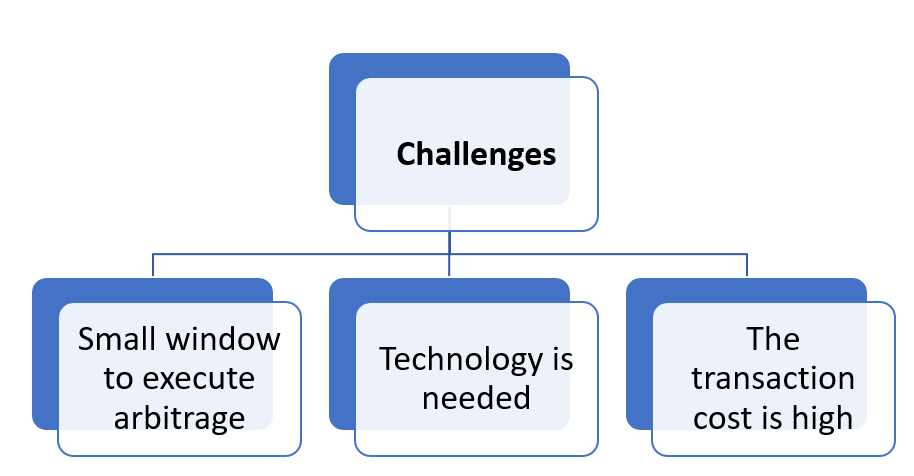

What challenges are associated with index arbitrage?

The arbitrage strategy seems very attractive to the retail investor as it promises easy money. However, the risk and reward balance should not be avoided. It is difficult to generate earnings from the index arbitrage, especially for the retail and individual investors because of the following reasons:

The window to execute arbitrage is small – The arbitrage trading must be executed in a very short span of time. It will difficult to execute a trade when someone is not utilising software and working manually. The price at which someone wants to sell, changes in no time and the opportunity can be lost and moreover, the trader can incur huge losses. As the trading volume is high, the loss can intensify. While trading through arbitrage, the time to think and execute the trade is very low, so actions should be taken quickly or through software.

Technology is needed – Through program trading the arbitrage opportunities can be located, and a trader can take advantage of the difference in the current and the future prices. For beginners, it is a difficult task to make accurate predictions manually. Series of calculations are undertaken by the statistical arbitragers to locate the opportunity. Therefore, the traders who cannot commit a lot of time to make a prediction should employ trading software.

The transaction cost is high – The arbitrage strategy involves simultaneous selling and buying of the stocks; therefore, the transaction cost is generally high. A transaction fee has to be paid for every single transaction, that is, the fee has to be paid for buying the security. Also, the transaction cost also depended upon the brokers. In many cases, the traders must restrict their arbitrage to a specific amount of shares because the transaction cost is higher than the profits.

What is the role of arbitrage in the market?

The function of the market is to bring the sellers and the buyers to a single place and set the prices. This process is termed price discovery. It might look like that the arbitrage is conducted to exploit the market inefficiencies, but in reality, it helps the market to keep the prices in line.

To illustrate: a future contract becomes overvalued as a piece of new information entered into the market and the traders overplay it. The arbitrageurs identify the overvalued future contract and start selling the same to make a profit. As a result, the price of the futures contracts is bought back to its original value.

Image source: © VectorMine | Megapixl.com

How arbitrage can be conducted in the market?

The arbitrage activity can be conducted in the options contracts to earn a profit, in two situations –

1 – When a discrepancy is observed in the put and call parity: If the concept of put call parity is violated, then it gives an arbitrage opportunity to the investors. To illustrate: Consider the scenario of an investor taking a long position in the future contract and in the put option. A call option is available for $20 and the put option on the same asset is available for $16. The difference of $4 is the cost of margin which an investor has to pay for taking a long position in the future contract. Here, there is no arbitrage opportunity. However, the arbitrage opportunity can arise, when the upside of the asset is seen as limited by the market participants. As a result, the cost of the call will come down from $20 to $14. The under-prices call option can be bought and the future and put option can be sold.

2 - Strike arbitrage: When two options with different strike prices on the same underlying asset are available, then the strike arbitrage can be conducted. The differences in the prices do not last for long because of the arbitrageurs.

To illustrate: the company’s share present value is $51, and its call option of $50 is trading at $1.50. Simultaneously, its $52 call option is trading at $3.00. Since the extrinsic value is exceeding the strike prices. Hence, a strike arbitrage is possible.

Please wait processing your request...

Please wait processing your request...