Definition – Implied Volatility

Implied volatility is typically defined as the gauge/measure of markets forecast on the possible movement in an asset/security’s price. The movement in price could be on account of market forces, or increased level of buying or selling.

An index such as VIX, which is based on the implied volatility of the S&P 500 index displays the market’s estimation of volatility of the underlying security in future.

Read: What Is Volatility?

There are two main types of volatility, i.e., historical volatility, which could be calculated by using recent trading activities of a stock or other security and are factual in nature, and forward-looking volatility, referred to as implied volatility.

The implied volatility component of option prices is the factor that can give all options traders, novice to expert, a hard time as the implied volatility of an option may change while all other pricing factors impacting the price of an option remain unchanged.

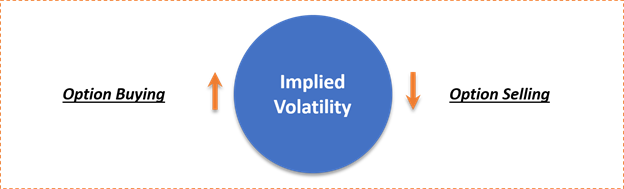

In general, a result of increased buying of options by market participants leads to higher implied volatility, and conversely, when there is net selling of options, the implied volatility indicated by option prices moves lower.

The implied volatility follows the basic fundamental principle of economics, i.e., a large options buying pushes it higher, and options selling pushes it lower, or simply, the implied volatility reacts to the basic demand and supply of the marketplace.

What are the Applications of Implied Volatility

Implied volatility of an option could be considered as a measure of risk in an underlying security, which pertains to the expected movement in the price of that security irrespective of its direction over the life of the option.

Moreover, while understanding the implied volatility and its application, it should be kept in mind that implied volatility only deals with the expected movement in an underlying stock and does not consider the direction of the movement.

Ideally, when investors consider risk, it is usually in terms of a stock falling in value. Implied volatility is similar to looking at the variance or the standard deviation of a mean value, as using it as a risk measure involves the estimation of the price either on the upside or down side.

For example, during a financial year, a company releases price-sensitive information, including the quarterly performance, news on Merger & Acquisition, product launch, etc. which may contain data that could assist investors in refining their forecasts regarding the company or re-value their investment.

Moreover, this information could have a considerable impact on the share price of the company under consideration, and in tandem, its option price, which usually trades on high premium; thus, are quick to adjust to new market information as a lot of anticipation is baked into option prices.

High demand for option pushes option prices up, and typically, a high price in options leads to high implied volatility. However, it would not be wrong to say that higher implied volatility leads to high option prices, either.

So, when the market anticipates a large move to the upside in the underlying security, it creates a high demand for call options in anticipation of this move, leading to an increase in option prices and its implied volatility.

Do read: Understanding Volatility; ASX VIX Spikes and Skyrockets 4x in a Month!

Likewise, if there is an expectation of a lower price move, the market may see an increase in put buying, and with higher demand for put contracts, the price of puts may increase resulting in higher implied volatility for those options as well.

An increase in put prices eventually pushes call prices at expiry due to a concept known as put-call parity, which serves as the foundation stone of understanding the ramification of implied volatility and estimating non-arbitrage option prices.

Put-Call Parity

Put and call are linked together through the price of an underlying stock via put-call parity, which exists because combining stock and put position can result in the same payoff as a position in a call option with a same strike price as the put.

The put-call parity is usually maintained in the market as any mispricing in prices create arbitrage opportunities, and usually, large funds or arbitragers seize this opportunity quickly to bring back the put-call parity in place.

Parity between the call and put results in a similar implied volatility output.

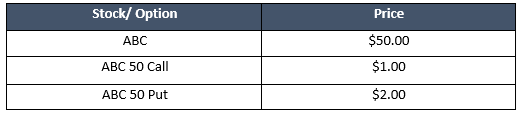

For example; consider a following situation

An investor can easily replicate the payout of long in ABC 50 Call by using the ABC 50 Put and ABC stock. The combination of owning a stock along with the put has the same payout structure as a long call option position.

With our ABC 50 Call trading at $1.00 and the ABC 50 Put price at $2.00, there may be a mispricing scenario.

Consider the following payout of combining Long Call, Long Stock, and Long Put.

Note, that in the table above, the combination of owning stock and owning a put should ideally have the same payout structure as a long call option. However, with the ABC 50 Call trading at $1.00 and the ABC 50 Put trading at $2.00, at any expiration, the long call position is worth $1.00 more than the combined stock and put position.

With this pricing difference, there is the ability to take a short position in the strategy that will be worth less and buy the strategy that will be worth more on expiry date.

Estimating Price Movement from Implied Volatility

What the implied volatility of an option projects onto the underlying security is the expected range of price movement over a certain period of time. This estimation of the expected price movement is based on statistics and the bell curve or the normal distribution curve.

The implied volatility of an option is the projection of an annualised one standard deviation move in the underlying stock over the life of an option.

To Know More About the Application and Calculation of VIX, Do Read: Implied Volatility- A Roadmap to Gauge Market Sentiment

Please wait processing your request...

Please wait processing your request...