What is Exchange Delivery Settlement Price (EDSP)?

Exchange Delivery Settlement Price is a delivery settlement price used by stock exchanges to calculate the amount of settlement of derivative contracts on an exchange. It refers to the amount at which contracts of exchange-traded derivative are settled.

Source: Copyright © 2021 Kalkine Media

Understanding Exchange Delivery Settlement Price

Exchange Delivery Settlement, or EDSP, it refers to the settlement price of a traded derivative. Stock exchanges use Exchange Delivery Settlement Price to measure the difference between the price of derivatives at the time of trade and its price at the time of expiry. This difference helps investors or traders to understand the extent of an open position whether it is out of the money or in the money. It helps to calculate the amount of an option or future contract at the time of its expiry and this amount owned by the concern parties. Exchange Delivery Settlement also refers to the final amount of cash according to its final agreement.

Frequently Asked Questions (FAQs)

How does exchange delivery settlement price interpret?

As discussed above, exchange delivery settlement price is the difference between the amount of traded derivative and its amount at the time of expiry. The difference shows us whether an option is in the money or out of the money. If the exchange delivery settlement price is higher in comparison of the price of the contract at the time of its expiry, it represents that the seller is out of money and the buyer is in the money. And if the exchange delivery settlement is less than the price of contract at the time of expiry than it shows seller is in the money and the buyer is out of money.

How does exchange delivery settlement price calculated?

The exchange delivery settlement price is calculated in several ways. The price’s calculation depends as per the market and exchange. It is calculation of the derivative contracts price in trade (exchange). Stock exchanges use different rates to calculate exchange delivery settlement price, some use a fixed rate from the third party, and other use calculation which is made by price date over a set time.

Like London Stock Exchange calculates the exchange delivery settlement price for the FTSE 100 through an auction. For each share of the index, it holds intraday auctions. For the last day of contract month, the exchange has an intricate list of rules which helps to keep the process transparent and helps in determining the average price weighted through most traded price.

How to determine exchange-related settlement prices on specific markets?

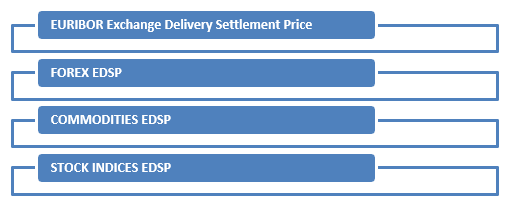

Exchange delivery settlement price is determined in different ways depending on specific market and exchange. The settlement price is calculated by using intricate data of price, which is difficult to understand for an individual. There are markets which determine exchange-related settlement prices by using their own ways of calculation including:

Source: Copyright © 2021 Kalkine Media

- EURIBOR Exchange Delivery Settlement Price

The exchange delivery settlement price is calculated by Euro Interbank Offered Rate which is a called daily reference rate. In the euro wholesale money market, Eurozone banks lend unsecured funds to other banks at averaged interest rates. This rate helps European Money Markets Institute to decide the Euro Interbank Offered Rate. Euribor future of three months will get its exchange delivery settlement price from Interbank Offered Rate. Rate set for the last trading day or a contract will use by Intercontinental Exchange (ICE), the corresponding futures exchange.

- FOREX EDSP

The Chicago Mercantile Exchange (CME) is using a complicated way to calculate the exchange delivery settlement price in a comparison to Intercontinental Exchange. Eurodollar futures contracts exchanged (traded) on CME, FX futures contract’s settlement price is calculated by using an intricate way. The Chicago Mercantile Exchange use 16 leading interdealer banks rates to measure the EDSP. It is calculated by taking average and discarding the lowest three and the highest three of the 16 rates. The exchange settlement price is calculated by put in the spread to the upcoming utmost liquid contract month. On the last trading day, the spread is traded within a 30-second’s window. The Chicago Mercantile uses the front and upcoming most liquid contract to get the weighted average price; it is used to find out the spread. The spread is used in the closing price of the upcoming month of contract. This calculation helps in determining the front contract’s delivery price.

- COMMODITIES EDSP

The exchange delivery settlement price of the West Texas Intermediate futures is determined by the market prices of the US light sweet crude and settled for the second last price per cask of crude. New York Mercantile Exchange published the prices, which are quoted in US dollar.

- STOCK INDICES EDSP

The Chicago Mercantile Exchange uses a different special opening quotation for US stock indices on the end of the trading day. The quotation takes more time to calculate because all stocks have different time of their opening. Special opening quotation is the exchange delivery settlement price of positions. Sometimes opening price of an index on the last trading day is different from the settled special quoting price. This method is used by the Chicago Mercantile Exchange for all indices including NASDAQ, EUREX Futures Exchange and S&P 500.

Please wait processing your request...

Please wait processing your request...