What is backflush costing?

Backflush costing or accounting is an approach in which the material usage is not recorded in the accounting books until the production process is completed. No journal entry records the work in progress inventory or the cost of raw materials while the production process is ongoing. Instead, a single journal entry is recorded at the end of the production process which records the total cost of production or manufacturing.

This process is useful for the organisations which have complex manufacturing process that involves various levels. In the normal accounting process, a journal entry has to be recorded separately for each stage of production to track the cost. It results in numerous journal entries for a single product. For the organisations that manufacture multiple products, it will result in a ton of unnecessary journal work.

The backflushing system avoids unnecessary journal entries and ensures that only useful information is recorded. However, the backflushing system might not be suitable for all product categories.

Summary

- Backflush costing or accounting is an approach in which the material usage cost is not recorder in the accounting books until the production process is completed.

- No journal entry records the work in progress inventory or cost of raw material during the production process.

- A single journal entry is recorded at the end of the production process which records the total cost of production or manufacturing.

Frequently asked questions (FAQs)

What are the features of backflush costing?

- The cost of material is not calculated separately during the production stage but is transferred to the account of the finished product cost.

- No separate work account is maintained to track the work in process.

- Until the completion of the production process or sale of a product, the journal entry process is delayed.

- The backflush accounting approach becomes inappropriate when the production process of an organisation is not limited to finished product manufacturing but also involves the production of parts along with variability in parts consumption.

- After the completion of the production process, the cost of the material is deducted from the total inventory, and the finished goods are recorded in the material account.

How does backflush costing work?

A standard cost is assigned to each unit of product manufactured by the organisation, to derive the cost per unit. After the completion of the manufacturing process, the number of manufactured units is multiplied by the standard cost and expenses are ascertained for recording a journal entry. The backflushing only takes place after the completion of the production process.

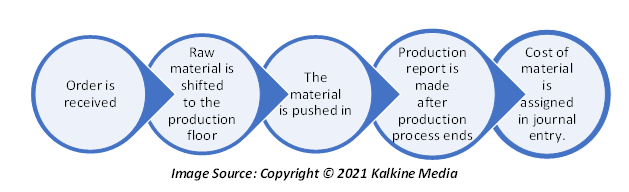

What is the Backflush costing process?

- The process marks its beginning when the company receives an order and all the essential details like quantity, item code and date of delivery are recorded. On the basis of the order, the list of raw material required is constructed.

- The raw material is shifted to the production floor for commencing the production process.

- After the company’s assessment regarding the raw material quantity and type, the material is pushed in.

- After the completion of the production process, all the details about the final products are entered into the system and a production report is generated by the software.

- Based on the production report, the cost of material is assigned in a single journal entry.

How is the journal entry for Backflush costing done?

The journal entries passed for backflush costing are as follows –

- The expenses are debited, and the payments are credited. If cash/ bank payment is made then cash or bank account is credited, similarly if the material is purchased on credit then the creditor’s account is credited.

- The finished goods account is debited along with the cost ascertained in the previous step.

- During the sale of finished goods, the cost of goods will be transferred in the account of the cost of goods sold and the finished goods account will be credited.

What is the difference between conventional and backflushing costing?

In the conventional costing approach, the raw material entry first is recorded in the raw material inventory account, then transfers to the work in process inventory and then into the finished goods account. In the backflushing costing, the raw material entry is only recorded when the production process completes and is directly entered into the finished goods account.

In the conventional costing method, the overhead and labour cost is recorded in the work in process account and then later moved to the finished goods account and lastly into the cost of goods sold. However, in the backflush costing method, all the costs related to the production are directly recorded in the cost of goods sold accounts.

When backflush costing should be used?

This costing approach is generally adopted by the companies which have low inventory holding period along with high turnover. The companies with slow inventory turnover record the cost when they occur as inventory might not be sold for a long duration and the cost recording can be incorrect on a future date.

It is most suitable for the manufacturing and production firms which deal with complex production processes, as backflushing simplifies the whole process of accounting. Companies that deal in product customisation do not adopt backflush costing as the cost per good can vary significantly.

What are the benefits of backflush costing?

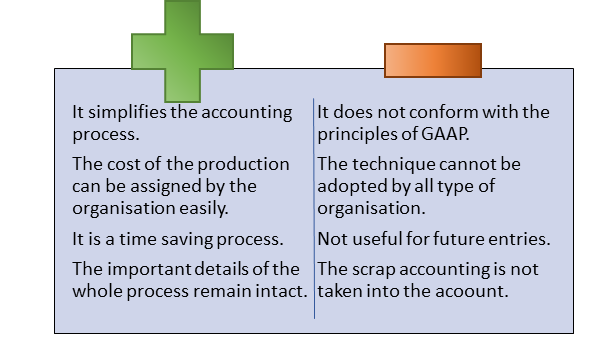

- It simplifies the accounting process of the organisation as the single journal entry is made and at the time of competition of production process, which further adds ease in calculations.

- The cost of the production can be assigned by the organisation easily for the corresponding inventory.

- It is time saving process for the data need not be updated on regular basis, as a result, it saves accounting costs too.

- The accounting process becomes easy for the bookkeepers and the important details of the whole process remain intact.

What are the drawbacks of backflush costing?

- The backflush accounting method may not be considered an ideal technique as it does not conform to the principles of GAAP.

- The technique cannot be adopted by all types of organisations, for example, it is not suitable for slow inventory turnover companies.

- The accounting entries for the standard cost may not be suitable for the entries in the future.

- The scrap accounting is not considered and in the production process, the scrap produced can accumulate into a large quantity. However, the material costs do not incorporate this scrap. Thus, these scraps need to be removed from the inventory to get the right picture.

Source: Copyright © 2021 Kalkine Media

Please wait processing your request...

Please wait processing your request...