Defined contribution plan vs IRA: Compare contribution limits, employer matching, Investment flexibility, tax benefits, and Retirement Planning strategies for US workers in 2026.

Key Highlights

- Defined contribution plans typically offer higher annual contribution limits and employer matching benefits.

- IRAs provide broader investment flexibility and greater account portability.

- Many retirement savers use both accounts to maximize tax advantages and long-term Wealth accumulation.

Defined Contribution Plan vs IRA: Understanding the Key Differences

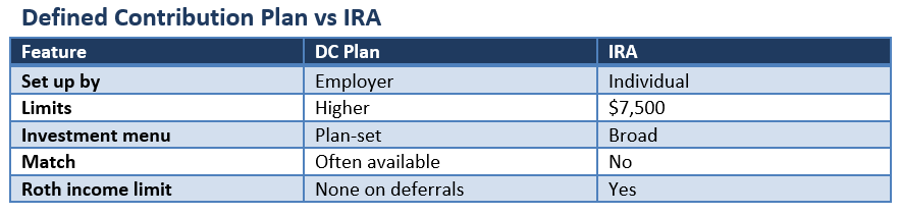

Retirement planning in the United States increasingly revolves around two major savings vehicles: employer-sponsored defined contribution (DC) plans and Individual Retirement Accounts (IRAs). While both are designed to help workers build retirement wealth, they differ significantly in contribution limits, investment choices, and employer involvement.

For many Americans, understanding these differences can help improve long-term retirement outcomes and optimize tax-efficient savings strategies.

What Is a Defined Contribution Plan?

A defined contribution plan is an employer-sponsored retirement arrangement where employees contribute a portion of their income into an investment account. Common examples include 401(k), 403(b), 457(b), and SIMPLE retirement plans.

Unlike traditional pensions, retirement income is not guaranteed. Instead, the Account Balance depends on contributions, investment performance, and market conditions over time.

One of the biggest advantages is that many employers provide matching contributions, effectively increasing retirement savings beyond an employee's own deposits.

How Does an IRA Work?

An IRA is a retirement account opened and controlled by an individual rather than an employer. Investors can choose between Traditional and Roth IRAs, each offering different tax benefits.

IRAs generally provide access to a wider range of investment Options than most workplace retirement plans. Investors can select from stocks, bonds, Exchange-traded funds, mutual funds, and, through specialized custodians, certain alternative Assets.

Because the account remains with the individual, it also offers greater portability throughout a person's career.

Contribution Limits Matter

One of the clearest distinctions between the two account types is annual contribution capacity.

For 2026, employee contributions to many workplace plans can reach $24,500, with total contribution limits significantly higher when employer contributions are included. By comparison, IRA contributions are generally capped at $7,500, with additional catch-up contributions available for eligible older savers.

For workers seeking to maximize retirement savings, defined contribution plans typically provide more room for tax-advantaged investing.

Investment Flexibility and Control

Investment choice is another major consideration.

Most employer-sponsored plans offer a limited menu selected by the plan administrator. These options often include mutual funds, target-date funds, and bond funds.

IRAs generally provide greater flexibility. Investors can choose from a broader universe of securities and may tailor portfolios to specific risk, income, or growth objectives.

This flexibility can be particularly valuable for experienced investors seeking customized retirement strategies.

Tax Benefits and Roth Features

Both defined contribution plans and IRAs can offer either traditional tax-deferred treatment or Roth-style after-tax contributions.

However, Roth IRA eligibility is subject to income-based phase-out rules. In contrast, Roth contributions within many workplace plans are generally available regardless of income level, making them attractive for higher earners seeking tax Diversification.

Why Many Americans Use Both

Rather than choosing one account over the other, many retirement savers use both.

A common strategy involves contributing enough to a workplace plan to capture any employer match, then supplementing retirement savings through an IRA for additional investment flexibility.

This approach can help diversify tax treatment, expand investment options, and increase overall retirement savings capacity.

Conclusion

Defined contribution plans and IRAs play complementary roles in modern retirement planning. Defined contribution plans often excel through higher contribution limits and employer matching opportunities, while IRAs provide broader investment flexibility and personal control. For many workers, combining both accounts can create a more diversified and resilient retirement strategy. As retirement rules and tax regulations continue to evolve, reviewing account choices with a qualified financial professional may help ensure retirement savings remain aligned with long-term goals.

Please wait processing your request...

Please wait processing your request...